-1.png?width=1169&height=277&name=Inovia%20Logo%20Dark%20(1)-1.png)

Methodology

It’s been nearly 5 years since Bristol-Myers Squibb (BMS) announced the mega-merger of Celegene for an eye-watering $74 billion. To this day, it is still one of the largest in the industry's history and this report looks at the successes and challenges of the merger. There is much discussion about how you can ever successfully integrate two companies with that stature of BMS and Celegene and therefore many questions remain on how successful the integration has been. At the time of the merger, there was significant changes in the industry, marked by a surge in M&A from other leading pharmaceuticals, such as Takeda's $62 billion acquisition of Shire in 2018 and AbbVie's $63 billion purchase of Allergan in 2019 as they looked to offset the impact of patent expirations on blockbuster drugs, we’re currently experiencing a similar scenario, with Merck, amongst others looking for other revenue streams with the looming Keytruda patent cliff.

During this time Oncology and Immunology showed the most promise, BMS wanted to strengthen its position in the space, and they believed Celgene offered just that. Initially, the merger came with scrutiny, not only from shareholders from both sides, but also the industry - ultimately who benefited most from the merger?

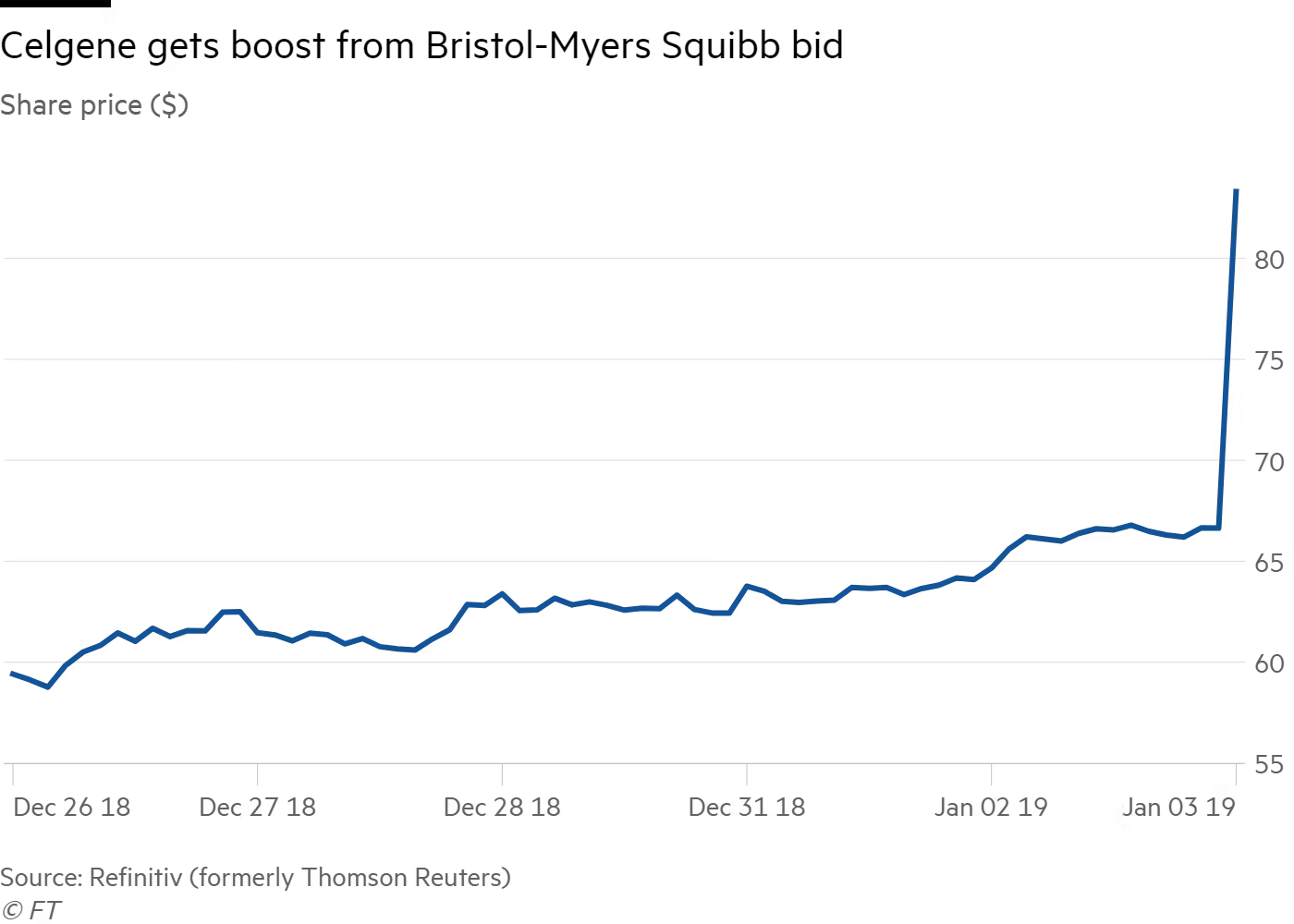

On April 12, 2019, BMS announced the completion of its merger with Celgene for a $74 billion stock-plus-cash deal. Pursuant to the terms of the merger agreement, for each share of Celgene stock, Celgene shareholders received one share of Bristol-Myers Squibb stock along with $50 in cash and one tradeable contingent value right, which entitled the holder to receive a payment of $9.00 in cash if certain future regulatory milestones were achieved, or $102.43 per share, a premium of 53.7% to Celgene’s close the day before. Celgene shareholders owned about 31 percent of the combined company at the time of the deal; subsequent changes such as buybacks have since decreased this. While Celgene was once one of the brightest stars in the industry, they faced one of the biggest patent cliffs in the industry, reflected in their stock performance, which fell more than 37% over the previous year. The announcement gave a boost to Celgene’s shareholders, with many seeing the deal as preferable for Celgene.

The deal added about $32 billion in fresh debt to BMS’s balance sheet, while also assuming $20 billion in Celgene’s debt, a large jump from BMS’s $7.3 billion outstanding debt at the time. The news sent the cost to insure Bristol’s bonds to their highest point since May 2010. As the price of long-term Bristol bonds fell, the associated credit default swap jumped 66 per cent, bringing the cost to insure $1 million of the company’s debt against default to $23,000, according to Reuters.

While Celgene’s investors were jubilant, BMS’s were less than enthused, with their share price sliding more than 12% after the announcement. Many of BMS’s investors felt the deal was overpriced, and at one point, there was skepticism whether the deal would be approved by shareholders following a survey by Mizuho Securities USA. Their largest institutional shareholder did not back the deal, owning around 8% of their stock. Wellington Management stated they were “not supportive of the company’s proposed acquisition of Celgene,” as it “does not believe that the Celgene transaction is an attractive path towards accomplishing this goal.” The deal was seen as a big win for Celgene, with concerns surrounding Revlimid, which brought in $2.5 billion the quarter before the merger, and how Celgene would replace the revenue once the patent ran out in 2022. It was no secret that Celgene had spoken to multiple other large pharmaceutical companies about an acquisition over the last year. The deal left Celgene and BMS with a combined 9 products, each with more than $1 billion in annual sales and significant potential for further products, with a diverse pipeline across Oncology, Immunology, and CV. “I think it’s impossible to predict whether this will be a successful deal or not, but I think it needed to happen for both companies,” said Loncar of Loncar Investments. “While there’s some disappointment in both camps, I think once the realism sets in, they’ll see both companies are in a better position because of this.”

Why did BMS want to acquire Celgene? They were most interested in acquiring Celgene’s blockbuster hematology immunomodulators, Revlimid and Pomalyst, combined with their late-stage assets such as Lisocabtagene maraleucel, JCAR017/liso-cel, and bb2121/ide-cel. BMS, up to this point, had major success in immuno-oncology and mainly solid tumors, with nivolumab providing substantial revenue. With a continued market share loss to Merck’s pembrolizumab, BMS looked for their next blockbuster in Hematology. Celgene also brought other assets such as luspatercept for anemia in myelodysplastic syndromes (MDS) and beta-thalassemia, as well as ozanimod for autoimmune diseases. BMS believed the merger would allow for a $2.5 billion annual cost saving by 2022 and ultimately improve efficiency and profitability; they confirmed they reached this target in 2021. The merger was also seen by some Wall Street analysts as a “defensive acquisition.” As mentioned earlier, there was a spate of M&A interest from other large pharmaceuticals, and there was a belief that BMS could be a target of a takeover. The acquisition of Celgene would increase their size, market share, and complexity, ultimately making them less attractive as a takeover prospect.

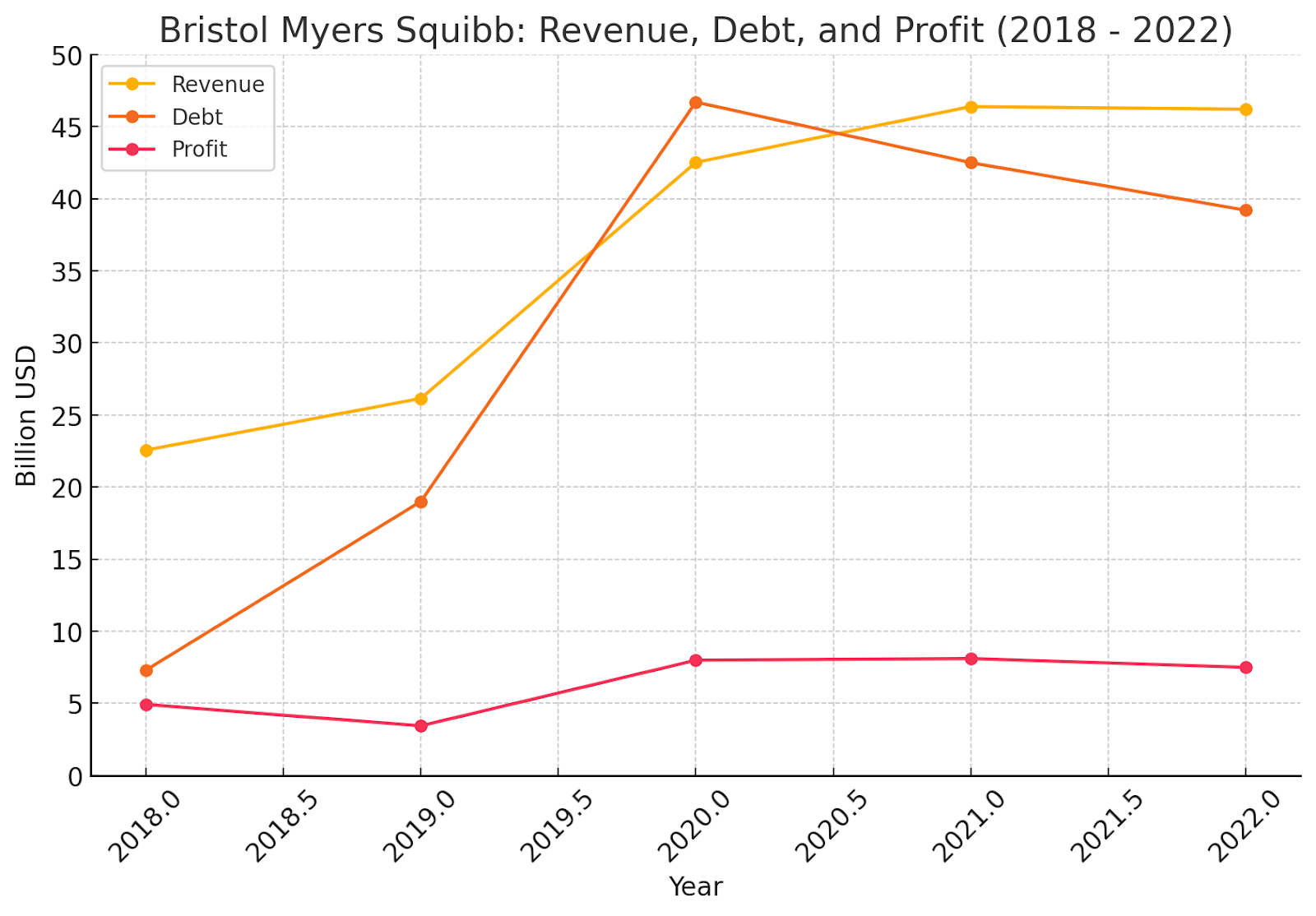

As we can see from the graph above, the merger had a significant impact on Bristol Myers Squibb’s (BMS) revenue and debt. Revenue rose sharply from $22.6 billion in 2018 (pre-merger) to $42.5 billion by 2020, driven by contributions from key Celgene products such as Revlimid and Pomalyst, despite challenges like the patent cliff. By 2021, revenue continued to grow, reaching $46.4 billion. To complete the merger, BMS took on substantial debt, which peaked in 2020 at $46.7 billion. Since then, the company has focused on paying down this debt, reducing it to $39.2 billion by 2022, partly using profits and proceeds from the sale of Otezla (Apremilast) to Amgen for $13.4 billion. Despite the revenue growth, profits were more modest due to the significant debt burden and integration costs. Profits dropped from $4.92 billion in 2018 to $3.44 billion in 2019 but then rebounded to around $8 billion by 2020. However, profits remained relatively stable at around $7.5 billion in 2022, reflecting the ongoing impact of debt servicing and integration expenses post-merger.

Integrating two companies the size of BMS and Celgene was never going to be easy, and the merger has led to subsequent challenges even to the present day, with the integration being described as a “journey” by Catherine Owen, BMS’ Senior Vice President of Major Markets. Many believe the integration of the two cultures was potentially the most difficult part of the merger, with Celgene adopting a “Biotech” thought process, with innovation and speed at the forefront, while BMS had a more thorough and bureaucratic approach. This, in combination with the $2.5 billion cost-cutting promise, led to a series of layoffs and management changes as they looked to streamline operations and reduce costs. Giovanni Caforio, BMS’ CEO at the time, wanted to reinvent BMS with Celgene, taking the best from each. While there was scepticism at the time, 5 years later, this has been partially successful. A merger would not be complete without a post-lawsuit, and in this case, that’s exactly what we got. The delay in the approval of lisocabtagene maraleucel led to a subsequent lawsuit as it affected a contingent value rights agreement worth up to $6.4 billion for Celgene shareholders. On October 1, 2024, a federal judge dismissed the lawsuit, stating UMB Bank, the plaintiff in the case, “had no standing to file a complaint against BMS because it had not been appropriately appointed as a trustee for shareholders who held these contingent value rights (CVR).”

When the merger was announced, it was almost impossible to guess if it would prove successful or not. Five years later, there have been challenges, especially with the integration of both companies. However, with hindsight, we can confidently say the merger has been more successful than many would have predicted. Ultimately, BMS has been able to launch nine products in the two years post-merger and also inherited some amazing talent. Therefore, success lies somewhere in the middle.

References:

https://www.pharmavoice.com/news/bristol-myers-squibbs-integration-celgene-catherine-owen/628485/

https://www.dcatvci.org/features/the-74-billion-marriage-of-bristol-myers-squibb-and-celgene/

https://pharmatimes.com/news/bms_competes_74bn_celgene_acquisition_1317844/